In the world of business, a perfect revolution occurs when the following three conditions are met. First, new market settings allow for a massive surge in capital growth. It can be related to technology, innovation, market expansion or some other factors.

Second, the way to create such value is so transformational only a new crop of high-performance organizations are able to capitalize on this new kind of growth.

Third, incumbent players have nowhere to go. Their only choice is to adapt or perish. Either way, they can’t use they market power to survive at the expense of other stakeholders.

Management and organizational history suggests there has been a number of these so called perfect revolutions. The Industrial Revolution at the end of the 19th century was certainly one of them. Industrialization brought massive capital growth. New industries and radically different organizations were born. Industrialists eventually freed us from feudal landlords and their economic and social shackles.

Later on, the scientific division of labour, the rise of the international financial system and the emergence of a body of knowledge in complex organizational management gave rise to conglomerates and multinationals; a trend which has since led to globalization.

Still, I believe one of the most perfect and transformational revolution to date has been the Digital Revolution. From its inception, it has generated massive capital growth mostly by altering the processes by which we think, create, transform, organize, act and transact amongst each other.

At the core of this revolution are players born relatively recently and more often than not out of a simple figment of imagination.

The intelligence and the programmetry embedded in their game-changing contributions, such as their intelligent devices, systems and end-users applications, have literally transformed just about everyone and everything.

Not in the least, the digital revolution has given rise to some of the best performing organizations ever to roam the face of the earth. Just as importantly, this revolution has also helped countless under performing organizations, including governments, to get their act together.

The case of the mobile telephony market

Sector-wise, the mobile telephony market has been one of the prime examples of the accomplishments related to the digital revolution. The amount of value realized in this market over the last decade is simply astounding. Thanks to the dynamic application marketplaces instituted by companies like Google and Apple, we have seen a massive influx of capital and new technologies which have culminated in a global race involving some of the most innovative players in the world. Thanks to them, we now have affordable advanced intelligent devices and applications at our becking call, which we wouldn’t have dreamt possible less than a decade ago. And it keeps going.

The point is, had we been stuck with the likes of Microsoft and its telecom peers, I dare to say this market would not have registered the type of phenomenal growth it has. There is a strong probability we would still be dealing with a bland, highly regulated and very much supply-sided oligopolistic environment in which customers needs and wants would not have been as well served.

Had it not been for this vibrant and competitive mobile marketplace, I doubt we would be currently conducting business and public transactions the way we are doing now nor that we would have benefited as much from the digital revolution. To see the rate at which these social, informational and transactional processes are now moving onto mobile platforms, I am inclined to think Apple, Google and the rest of them did a lot more in harnessing the new economy than we give them credit for.

Another important consideration when discussing about the virtues of the mobile revolution, as well as the digital revolution at large, relates to the role of governments and regulators. Had they continued to act as pushovers and slow-movers like they did in the past, I believe we would still be at the mercy of incumbents who would have never been able to conduct their business in a similar fashion has the new players did.

Instead of focussing their efforts in creating real value like the new players had to in order to break their stranglehold, I think the incumbents would still be playing politics and leveraging the fallacies of protecting their outdated technologies, product lines, their centralized organizations and old classification jobs. They would also be doing all they can to preserve the economic privileges of their management and shareholders. And, we wouldn’t have seen as much investment in next-generation companies and new quality jobs, which have since become important components to our economy and our society.

Why is education heading for a perfect revolution?

When I look at the education sector these days, I can’t resist drawing a parallel with what the telephony market was back in the days when it was solely in the hands of a few similarly minded suppliers and network providers. I also see the same three reasons why education is heading for a revolution of its own. I see an untapped reservoir of colossal value which will soon be up for grabs. I see game-changing players coming after this strategic market with no holds barred and with all the intentions of replicating, improving, or at least be part of, what Apple, Google and others did in the mobile market. Finally, I see incumbent education networks having the same structural difficulties, if not considerably more, to retain their clientèle and the support of their respective government.

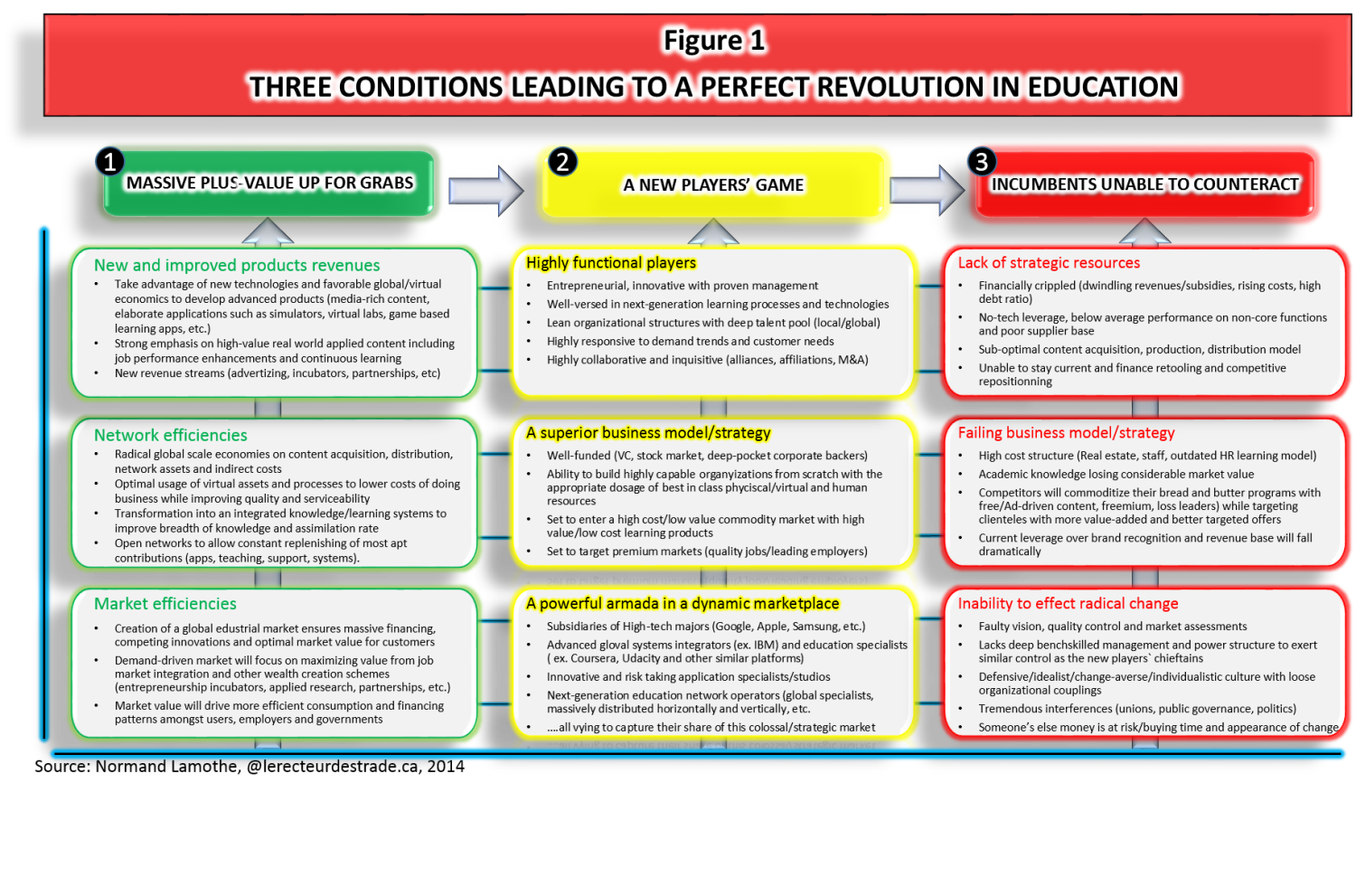

Figure 1 provides an overview of the three conditions and the nine legitimate reasons leading to what we foresee as a perfect revolution in education. (click on figure to enlarge).

1. An untapped reservoir of colossal value

As the left column in figure 1 suggests, I see three reasons why we should expect a massive surge of capital growth in the education sector over the coming years.

First of all, I believe we are in for a massive uptake in terms of new and improved product revenues. The explanation is simple. On the one hand, we have a wide range of advanced technologies making their entry in the world of education. On the other hand, we have scale economies related to the scalability of virtual assets and global market expansion which are bound to radically alter the cost structure of content production, distribution and just about every other learning processes.

It is our contention that these new technologies and economic drivers will give rise to a global edustrial application marketplace similar to the ones we have seen emerging in the mobile market as well as in other sectors (computing, media, e-commerce, etc.). Just as we have seen in aforementioned markets, we think this global marketplace will in turn trigger an explosion of sophisticated educational applications and systems. Indeed, we expect the relatively bland education products we now have to be eventually replaced with rich media content and sophisticated applications and processes such as advanced learning simulators, virtual reality classes, serious games, adaptive learning, artificial intelligence-based personal learning digital assistants, integrated learning support platforms which will provide optimal use of human, physical and virtual assets to maximize learning and assimilation.

As a result of these developments, we believe expect a major revenue shift from the old to the new product environment. While new players will compete to capture the extra value in these new developments, we expect current education systems to suffer from commoditization and a radical downshift in the demand for traditional academic products.

Besides this major shift toward new and improved products and services, we expect new players to derive significant value from maximizing network efficiencies. In my view, gone are the days of closed-contributions education networks based on the lifelong tenure. I expect the next crop of education providers to fall into the category of open networks. By that we mean networks built on the premises that in order to compete they will need to provide an open and dynamic access to the best available resources worldwide.

They will also need to configure their networks to provide an optimal dosage of virtual, physical and human resources so as to offer maximum flexibility, optimal access and support as well as cost efficiencies.

We also expect the value chain of these new networks to be less about traditional teaching and more about providing providing a highly efficient integrated learning environment. That means investing a great deal more in content acquisition, distribution and learning support.

There is finally a third area of value creation the next-generation education networks will try to pursue to their advantage. It relates to market efficiencies. We see two important value drivers being sought in this regard. First, we expect next-gen networks to focus their efforts on creating a much superior education to employment (EtoE) experience. An experience which will allow them to put their strategic advantage in new resources acquisition to good use while differentiating themselves from the often abstract and out-of context academic-based teaching traditional education networks currently bring to the table.

The main reason behind this first strategic focus is simple. No matter the mantra about the virtues of general education – which is often code for faculties to present their abstract representation of the world – EtoE is where lies the real value lies for the vast majority of learners. It provides them with a much better chance to build themselves as complete individuals. It offers them the chances to access quality job markets, to rise faster and earn a more rewarding living compared to what the majority of us can do after going through a typical book smart academic learning trajectory.

Secondly, we expect next-generation education and training networks to focus a great chunk of their efforts on the lifelong/lifewide learning opportunity. Again, the reasons are simple. With people getting older, quality jobs being sourced at the global level and job markets getting tougher and more competitive than they have ever been, it means people will not only need to work longer, they will also need to work smarter. Knowing this clientèle already has money in their pockets, and a revenue stream to protect, it seems pretty clear that we a have high probability to see a major uptake in the demand for real-time/on-the-job performance and lifelong career enhancements. That is of course a market that will only be accessible to the next-gen networks who will find the best way to come up with proven and actionable real-world learning. Personally, I believe we are looking here at two segments that will eventually be the tail that wags the dog. However, for that to happen, I’ll let you imagine the kind of radical changes this type of real education will entail in terms of expertise, content and network characteristics. I believe the answer to that question is likely to give us a hint as to who stand to gain the most in the future knowing where the real value is.

2. A new players’ game

Even though the edustrial marketplace and the next-generation education network providers are clearly in the early stage – with its high rate of unsustainable births, technological mirages, pipe dreams and dumbstruck learning and business models such as MOOCS – there are no less clear indications this marketplace is in the process of solidifying itself.

Just as we saw during the emergence of the computing, the video games or the internet-based industries, we believe all the major ingredients are being put in place so that we will see the emergence of players as agile, resilient, innovative and powerful as the ones we now see in the aforementioned sectors.

We have leapfrogging technologies, scale economics and deep pocket players already committing vast technical and financial resources with the hope of getting their fair share of this colossal strategic sector. We have players amongst the smartest, most innovative and capable on the planet who understand quite well what is at stake and who believe a powerful armada of companies coupled with a new dynamic marketplace will sooner than later transcend – in terms of raw talent, quality, attractiveness, costs, scalability and usefulness – what is being currently offered by bogged-down traditional systems. They know that once their capabilities go online, their takeover of the sector will be a mere formality as learners and employers alike will quickly go their way. From that moment, governments will have no choice but claim their own financial advantages of having these new players around to lower the cost of education and ensure we bring our economy and society in sync with what the best practices around the world.

3. The demise of incumbent players

Finally, as the third column in figure 1 suggests, we think education is heading for a much needed revolution because the level of market power we have allowed our current national education systems to have over the years, simply don’t match any more the kind of productivity we need from them in this brave new world. We see three reasons for the need of such a major overhaul.

First, however instrumental and well-intentioned they have been and still are, and no matter they are willing they are to change, the hard truth is our education systems simply lack the strategic resources to reposition themselves in such a fast-pace and costly environment.

Except for the schools who benefit from a privileged clientèle and a closed pairing with leading employers, such as business and engineering schools, most organizations are in no financial position to sustain any kind of transformational change. And that problem is only going to get worse.

With globalization and consolidation set to hit across the vast majority of our national industrial grids, most governments will have to deal with a major downshift in fiscal revenues. This means no matter how big a priority education is for them, our systems will simply not have the financial resources they need to retool themselves. Especially knowing older generations now clearly hold the balance of political power in most industrialized countries and are more preoccupied with their age related issues (health, revenue security, economic growth, etc.).

Just as importantly, we need to realize our education systems no only don’t have the money, they also lack the technological know-how, the supplier base, the next-generation content and the same efficient distribution infrastructures their new competitors will have.

As if that wasn’t enough of a problem, their business models are about to be commoditized. Their bread and butters programs will soon be faced with way more sophisticated content and cheaper alternatives. Coupled with the financial problems we just alluded to, the prospect of losing major chunks of revenues, especially their high-end clientèle to better players, does indeed pose a major business threat.

Add to this the fact that we are dealing with incumbents historically caught up in their secular ways of thinking and doing things; the fact that we have education managers who have not been groomed to think outside the box; the fact that we have institutions which organizational framework are characterized by extreme rigidities (the politics of academic and bureaucratic fiefdoms, powerful unions and political interference; it seems pretty clear we have a high probability the incumbent networks will have a hard time, to say the least, to commit to any kind of meaningful change within an appropriate time frame.

Finally, let’s not forget that we are dealing with a sector who is currently in a position to use whatever governance leeway it still has to delay the inevitable. Despite what should be already construed as a failed model, the sector still enjoys a strong institutional aura. It has influential advisory boards who are in a position to sell the illusion of change. They have enough a big revenue-base to direct some of it toward second-tier integrators and vendors who will be more than happy to oblige them with whatever projects they can sell based on the notion they will bring on equal footings with the new players, or at least integrate their developments and preserve their existence.

As we have across so many sectors in the past, and within so many bellwether corporations that have since disappear, there is a strong probability our education systems will go down this fancy path and end up wasting considerable money while postponing the hard decisions they need to make, including letting more apt players take over. Unfortunately for us, the repercussions are quite different than what usually happen in the private sector. Here we all stand to lose from people buying time at everyone’s expense, not just shareholders who are risking their own money.

Conclusion

There is very little doubt that a revolution is coming to the world of education. How will this plays out and how soon this new edustrial marketplace and these next-generation education networks will take over remains to be seen. But, a number of things should already be considered with a fairly high degree of certainty.

First, we believe the plus-value provided by this new global application market will prove real. And so will the performance derived from future network and market efficiencies.

Second, all indications are that new players are doing what needs to be done to emerge at the top of this new global marketplace. Contrary to popular beliefs, they are not just selling intelligent devices, building infrastructures to offer free online classes. Nor are they dedicated to create the teachers or the classes of the 21st century. It goes way deeper than that.

Third, the way things are progressing right now, I am not seeing the incumbent systems committing to the kind of changes that could warrant their future existence. Full disclosure, I don’t think they can. Personally, I have yet to see a sector so bogged down by its internal power structure and its lack of experience and strategic resources.

Of course, I could be wrong. That being said, and with so much plus-value up for grabs and powerful players knocking down the gates, I believe it would be ill-advised to blindly trust incumbents to control the vision, the decision process and the financial means. I would rather suggest this to be the perfect time to build new bridges and to back and foster players who clearly have the right DNA to strive in this next-generation global education marketplace.

Strategy-wise, it is all the more important we do so since we have all the reasons to believe that learning and training will be a key to the future and certainly one the best ways to stay in sync with a global economy which promises to be far less accommodating to those who lag behind. Hopefully, we can ride this global wave rather than be caught by it.